Zara Larsson has shared her experiences successful a Swedish expertise present aged 10.

In a brand new interview with The Guardian, Larsson opened up about successful Talang as a younger little one, and its affect on her music profession. Talang is a part of the favored Bought Expertise sequence, and Larsson gained together with her rendition of Celine Dion‘s ‘My Coronary heart Will Go On’.

“Again then, I by no means actually had any worries or doubts about being profitable, as a result of I knew deep in my soul that I used to be destined to be an entertainer, which is why I entered Talang,” Larsson shared. “The one factor I used to be frightened about was the pace with which I’d get that success.

“After the present, I thought it could be like: growth! I’m going to get signed, I’m going to be a celebrity! However nothing occurred for 4 years.

“I discovered that very nerve-racking, and frightened my profession is likely to be over. I went again to normality.”

Larsson just lately launched her new album ‘Venus‘, and spoke to NMEconcerning the album in a brand new interview earlier this month. She opened up about collaborating with producer Rick Nowels (whose credit additionally embody Madonna and Lana Del Rey).

“Rick is a really, very, very cussed individual and so am I,” she stated. “He would say, ‘I don’t like that,’ and I might say, ‘Effectively, I like that.’ We might do this backwards and forwards,’” she continues. “At first, it was exhausting to vibe with him, however… he’s particular. I realized a lot about myself and songwriting. I actually loved that he anticipated stuff from me. He held me to a typical that I wish to be held to.”

She additionally spoke to NME in 2023, the place we requested her whether or not she was open to taking part in Eurovision: “It’s nonetheless a no! However I might like to be an interval act.

“I’m a very massive fan of Eurovision, I watch it yearly,” she continued. “Eurovision and [our national selection show] Melodifestivalen are an enormous a part of Swedish tradition, and my boyfriend dances on that present yearly. So yeah, I’d like to be a part of it, however I don’t suppose I might wish to be a part of the competitors.

“I’m additionally actually scared as a result of, like, I’m doing fairly nicely in my life [and as] an artist. However what would occur if I [entered Eurovision and] didn’t get to the finals and so they simply voted me out? I really feel like it could be like, ‘Oh wow, that’s the tip of my profession!’”

Larsson is halfway by means of her UK and Eire tour – check out any remaining tickets right here and take a look at remaining dates under:

FEBRUARY 18 – O2 Academy, Birmingham 21 – Roundhouse, London

Small enterprise homeowners and their stakeholders are sometimes comfy with the established order. In any case, why rock the boat if issues are working proper? Nevertheless, you want to combine issues up and embrace change if you need your small enterprise to develop and thrive. In any other case, chances are you’ll be left behind, as loads of retail retailer homeowners, journey brokers, and newspaper publishers can attest.

To find alternatives for change and development, take into account appointing a selected group member as your “Disrupter in Chief.” This information, complemented by knowledgeable insights, gives methods to determine and empower such a frontrunner. It ensures your small business adapts and leads in innovation inside your trade.

What’s a Disrupter in Chief?

A Disrupter in Chief (DC) for small companies is a stakeholder inside that group who performs a pivotal function in driving optimistic change and innovation. This particular person is liable for difficult the prevailing norms and processes inside a corporation to foster development and flexibility.

By questioning the established order, the Disrupter in Chief encourages the enterprise to discover new concepts, methods, and methodologies that may result in important developments and aggressive benefits.

Michael Haddon, CEO of the enterprise software program firm Kradle, gives additional perception into this function. In an electronic mail interview with Small Enterprise Tendencies, Haddon described a DC as “a stakeholder in a enterprise who conjures up and helps optimistic change by difficult the established order.”

This definition underscores the significance of getting somebody inside the group who is devoted to steering the enterprise towards continuous enchancment and innovation, making certain it stays dynamic and aware of the ever-changing enterprise panorama.

Why You May Want a Disruptor in Chief

Haddon additionally shared some insights on why this place will be so useful for small companies. Listed here are the highest the explanation why you need to take into account including a DC to your group.

You Have to Change However Are Afraid to Do So

Change is important for any rising enterprise. Nevertheless it additionally represents a major quantity of threat. So many entrepreneurs merely hope to develop with out taking that essential threat that goes together with it.

Haddon says,

“As companies evolve, usually the largest hurdle to future success is an unwillingness to alter – or the need to maintain doing issues the identical method as they’ve at all times been executed. For example, primarily based on analysis we commissioned in 2018 (a complete survey of 700 small to medium enterprises (SMEs) throughout USA, UK and Australia), we discovered that 76% of companies within the US want to develop. Nevertheless, solely 27% of those self same companies anticipated change within the subsequent 12 months. A DinC embodies the 27% of companies that acknowledge that with a view to develop, change should happen.”

You Want Somebody to be Proactive in Making Change Occur

Even in the event you’re open to alter, you may not have the ability to put sufficient concentrate on looking for these alternatives when you’re busy working the entire different facets of your small business. A disruptor in chief is usually a choice maker inside your group or an influencer or advisor whose sole focus is on discovering these alternatives proactively so that you just and the opposite members of your group can focus in your particular duties whereas nonetheless with the ability to make the most of development alternatives as they arrive up.

Haddon says, “They acknowledge gaps and alternatives, and so they use that information to take it upon themselves to enhance the enterprise. This may very well be by creating and driving a brand new development technique primarily based on market modifications, figuring out inefficiencies inside the operations of a enterprise, inspiring employees to be extra productive and constant to the enterprise, or figuring out revolutionary applied sciences that may enhance the enterprise. In a nutshell, a DC is proactive and at all times in search of new methods to constantly enhance any facet of a enterprise.”

You Want Somebody to Encourage Others

Along with being proactive, a DC additionally must be educated, pushed and in a position to encourage others. That last high quality can actually assist companies form their tradition into one the place change and innovation are embraced, fostering much more development alternatives than one particular person can lead you to.

Haddon provides, “These traits as an entire bundle will be onerous to return by – as mirrored in our analysis which rated discovering high expertise because the third best problem for SMEs – as they don’t at all times come naturally. These traits will also be taught to the appropriate individuals and additional nurtured by the appropriate mentors/leaders. Companies have to spend money on their employees to carry out the very best in them, not merely search to rent perfection. An irreplaceable high quality is angle. In the event that they lead by instance, others will observe. In any case, diamonds don’t begin out shining.”

Challenges in Small Enterprise

Position of a Disruptor in Chief (DC)

Concern of Change

Overcoming concern of change

Proactive Change Administration

Figuring out alternatives proactively

Inspiration and Management

Fostering a tradition of innovation

Bridging the Expertise Hole

Nurturing worthwhile traits

Investing in Workers Growth

Constructing a talented workforce

Main by Instance

Setting a optimistic instance

Embracing Change with a Disrupter in Chief

In at present’s quickly evolving enterprise panorama, embracing change is essential for small companies to thrive and develop. To navigate these shifts successfully, take into account appointing a Disrupter in Chief inside your group. Right here’s why this function is usually a game-changer to your small enterprise:

Overcoming the Concern of Change: Change usually includes dangers, and plenty of entrepreneurs hesitate to embrace it. Nevertheless, stagnant processes can hinder development. A Disrupter in Chief embodies the braveness to problem the established order and acknowledges that change is important for future success.

Proactive Change Administration: Small enterprise homeowners have quite a few tasks, making it difficult to proactively search development alternatives. A DC can focus solely on figuring out gaps and alternatives, driving development methods, enhancing operations, and provoking productiveness, making certain that change occurs effectively.

Inspiring Innovation: A profitable Disrupter in Chief shouldn’t be solely proactive but in addition inspiring. They possess the information and drive to encourage others inside the group. This high quality can foster a tradition of innovation and alter acceptance, paving the way in which for extra development alternatives.

Facilitating Strategic Resolution-Making: With a DC in place, companies can higher navigate the complexities of the trendy market. This function aids in making knowledgeable, strategic choices by analyzing developments, knowledge, and alternatives, thus steering the corporate towards long-term success.

Enhancing Aggressive Edge: By constantly searching for and implementing revolutionary options, a Disrupter in Chief helps preserve and improve the corporate’s aggressive edge. This ensures the enterprise stays related and forward of trade shifts, securing its place out there.

Implementing a Disrupter in Chief Successfully

When you’ve acknowledged the necessity for a disrupter in chief in your group, it’s important to make sure a easy integration of this function. Right here’s a information to implementing yours successfully:

Clear Position Definition: Outline the DC’s tasks, authority, and scope inside your group. Be sure that their function aligns with your small business’s development aims and challenges.

Recruitment or Choice: Establish people inside your group who exhibit the qualities of a disruptor or take into account exterior candidates who carry contemporary views. Search for people who’re proactive, revolutionary, and able to inspiring change.

Coaching and Growth: If essential, present coaching and growth alternatives to nurture the DC’s expertise. This will embody management, innovation, and alter administration coaching.

Integration into Groups: Combine the DC into your present groups, making certain they’ve entry to related info and stakeholders. Encourage collaboration and open communication.

Common Reporting: Set up a reporting construction that enables the DC to often replace management on potential alternatives, challenges, and progress towards implementing modifications.

Measuring Success: Outline key efficiency indicators (KPIs) to measure the DC’s impression in your group’s development and flexibility. Recurrently assessment and assess their contributions.

Domesticate a Tradition of Change: Encourage a tradition the place workers in any respect ranges are open to alter and innovation. The DC can play a significant function in fostering this tradition.

Help and Sources: Present the required assets, together with budgets and instruments, to empower the DC in driving optimistic change.

Steady Enchancment: Acknowledge that the function of a DC evolves over time. Encourage ongoing studying and adaptation to remain forward in a dynamic enterprise atmosphere.

Empowering Your Disrupter in Chief

To maximise the effectiveness of your Disrupter in Chief and guarantee they drive optimistic change inside your small enterprise, take into account the next methods:

Clear Communication: Set up open and clear channels of communication together with your DC. Encourage them to share their insights, concepts, and findings with all the group. Create an atmosphere the place everybody feels comfy expressing their ideas on potential modifications.

Steady Studying: Put money into the skilled growth of your DC. Help them in buying new expertise, staying up to date on trade developments, and attending related workshops or coaching packages. A well-informed DC is best outfitted to determine alternatives for enchancment.

Collaborative Strategy: Foster collaboration between your DC and different group members. Encourage cross-functional groups to work collectively on initiatives associated to innovation and alter. This collaborative effort can result in holistic options and extra profitable implementations.

Useful resource Allocation: Present your DC with the required assets and instruments to discover and implement modifications. Whether or not it’s budgetary assist, entry to analysis supplies, or expertise options, guarantee they’ve what they should drive innovation.

Metrics and Accountability: Outline clear metrics and key efficiency indicators (KPIs) to measure the impression of modifications proposed and executed by your DC. Maintain them accountable for reaching particular objectives associated to enterprise development, effectivity, or buyer satisfaction.

Suggestions Loop: Set up a suggestions mechanism the place workers and clients can present enter on proposed modifications. Your DC can use this worthwhile suggestions to refine methods and make data-driven choices.

Recognition and Reward: Acknowledge and reward the efforts and successes of your DC and their group. Rejoice milestones, improvements, and optimistic outcomes ensuing from their disruptive initiatives. This recognition can increase morale and motivation.

Adaptability Coaching: Provide adaptability coaching to your complete workforce. Assist workers embrace change, adapt to new processes, and perceive the advantages of innovation. This may create a extra change-ready atmosphere.

Lengthy-Time period Imaginative and prescient: Work together with your DC to develop a long-term imaginative and prescient to your small enterprise. Align this imaginative and prescient together with your core values and mission, making certain that each one modifications contribute to your total strategic objectives.

Common Critiques: Conduct common critiques and assessments of the disruptive initiatives undertaken by your DC. Consider the impression on the enterprise, buyer satisfaction, and worker engagement. Modify methods as wanted primarily based on these assessments.

Key Perception

Actionable Technique

Clear Communication

Set up clear channels for sharing insights.

Encourage team-wide thought expression.

Create an open atmosphere for discussing potential modifications.

Steady Studying

Put money into the DC’s skilled growth.

Help talent acquisition and trade consciousness.

Encourage attendance at related workshops and coaching.

Collaborative Strategy

Foster cross-functional teamwork on innovation initiatives.

Promote synergy for holistic options.

Drive profitable implementation via collaboration.

Useful resource Allocation

Present budgetary assist for innovation endeavors.

Guarantee entry to important analysis supplies.

Equip the DC with essential instruments and applied sciences.

Metrics and Accountability

Outline measurable KPIs for assessing change impression.

Maintain the DC accountable for reaching objectives.

Consider their contribution to enterprise development.

Suggestions Loop

Set up mechanisms for worker and buyer enter.

Make the most of worthwhile suggestions to refine methods.

Make data-driven choices to enhance modifications.

Recognition and Reward

Rejoice DC-led milestones and improvements.

Enhance group morale and motivation.

Reinforce a tradition of innovation and optimistic outcomes.

Adaptability Coaching

Provide adaptability coaching for all the workforce.

Put together workers to embrace change.

Foster understanding of the advantages of innovation.

Lengthy-Time period Imaginative and prescient

Develop a strategic, mission-aligned imaginative and prescient for the enterprise.

Guarantee modifications align with core values.

Hold long-term objectives in thoughts when implementing modifications.

Common Critiques

Conduct ongoing assessments of DC-led initiatives.

Modify methods primarily based on evaluations.

Guarantee alignment with enterprise, buyer, and worker wants.

Conclusion

In conclusion, embracing change and innovation is paramount for the expansion and success of any small enterprise. The function of a Disrupter in Chief (DC) is usually a game-changer on this pursuit. A DC brings a singular mix of proactivity, innovation, and inspiration to the group, making them instrumental in figuring out alternatives, driving optimistic change, and fostering a tradition of adaptability.

Small companies usually face the problem of resisting change as a consequence of threat aversion or useful resource constraints. Nevertheless, as demonstrated by the analysis, the willingness to embrace change is a crucial think about reaching development. A DC embodies this willingness and actively seeks out methods to enhance numerous facets of the enterprise, from operational effectivity to market methods.

Furthermore, a DC’s function extends past merely recognizing alternatives; they encourage and lead by instance, motivating others to affix within the pursuit of innovation. By nurturing these qualities in your group and investing in your employees’s development, you possibly can create an atmosphere the place optimistic change shouldn’t be solely welcomed however embraced.

As you take into account integrating a Disrupter in Chief into your small enterprise, keep in mind that their success depends on clear function definition, steady growth, and seamless integration into your groups. Common evaluation of their impression and the cultivation of a tradition of change are equally important.

In a quickly evolving enterprise panorama, staying stagnant shouldn’t be an choice. Small companies that harness the facility of a DC and champion change can be higher outfitted to navigate challenges, seize alternatives, and thrive within the ever-changing market. Embracing change at present can safe a affluent tomorrow to your small enterprise.

Understanding the price of a million-dollar life insurance coverage coverage might be pivotal in securing your loved ones’s monetary future. However have you ever ever puzzled simply how accessible or pricey such a coverage is perhaps?

Do you suppose a million-dollar time period life insurance coverage coverage appears like an excessive amount of insurance coverage?

As a Licensed Monetary Planner, I see underinsured folks day by day.

What do I inform them?

One million-dollar time period life insurance coverage coverage would possibly truly be the minimal protection wanted for the standard middle-class family, but it surely’s reasonably priced.

That may sound like an exaggeration, however should you crunch the numbers – simply as we’ll be doing a little bit bit – you’ll notice {that a} million-dollar coverage is perhaps simply what you want.

What makes time period life insurance coverage even higher is that bigger insurance policies value much less on a per thousand foundation than smaller insurance policies do. It’s possible you’ll discover the premium on a $1 million coverage is barely a little bit bit increased than it’s for $500,000.

Do You Actually Want a $1 Million Time period Life Insurance coverage Coverage?

In all probability, however let’s discover out. A normal rule of thumb is that it is best to get 10x your revenue as baseline protection for all times insurance coverage.

For those who’re younger, which may be low as a result of chances are you’ll need to present your loved ones with sufficient to interchange your revenue for 15 years or extra.

Immediately, $1 million has change into the brand new baseline forlife insurance coverage by a major breadwinner. Something much less may depart your loved ones financially impaired.

Typical Obligations to Add When Calculating the Quantity You Want

Right here’s a listing of all of the totally different obligations chances are you’ll need to have life insurance coverage cowl within the unlucky occasion you go away early.

Your Earnings (And for How Many Years)

Any Debt You Might Need to Be Settled

Future Obligations Equivalent to School for Youngsters

Different Obligations Equivalent to Enterprise

Typical Objects You Can Subtract When Calculating the Quantity You Want

Present Life Insurance coverage Insurance policies

Belongings (Like Money or Inventory) You Would possibly Select to Use As an alternative of Life Insurance coverage

Now that you’ve got an thought of those obligations, let’s punch them into this life insurance coverage calculator to search out out should you want a million-dollar coverage.

Selecting A Million Greenback Insurance coverage Coverage

In response to CoverageGenius, the typical value for a 20-year $1 million time period life insurance coverage coverage for a 35-year-old male is $53 monthly. Nonetheless, your fee will differ in line with the next elements.

Elements that have an effect on your fee:

Your Protection Quantity and Coverage Time period

The place to begin?

The very best, and best place to begin is on-line. I like to recommend having two or three insurers compete for your small business to be sure you get the most effective fee and protection. To see how low-cost time period life might be, select your state from the map above to be matched with prime life insurance coverage suppliers immediately.

Elements That Have an effect on How A lot You Want

Let’s take a look at the person parts that may shortly add as much as over a million-dollar coverage.

Earnings Substitute

That is the place issues can get a bit intimidating. Even should you earn a modest revenue, chances are you'll want near $1 million to interchange that revenue after your loss of life with a purpose to present for your loved ones’s fundamental dwelling bills.

The standard knowledge within the insurance coverage business is that it is best to keep a life insurance coverage coverage equal to between 10 occasions and 20 occasions your annual revenue. So should you earn round $50K per 12 months, that might imply coverage protection between $500K and $1 million.

The complication at the moment is that with rates of interest being as little as they're that may not be sufficient both.

For instance, in case you have a $1 million coverage that might be invested at 5% per 12 months, your loved ones may stay on the curiosity earned – which conveniently involves $50,000 per 12 months – for the following 20 years.

That will nonetheless depart the unique $1 million intact to cowl different bills. However with at the moment’s microscopic rates of interest, there’s no solution to get a assured return of 5% in your cash, definitely not for 15 or 20 years.

EXPERT TIP

That brings us again to simple arithmetic – multiplying your annual revenue occasions the variety of years your loved ones’s dwelling bills will must be lined. This alone can require a $1 million life insurance coverage coverage.

Additionally, needless to say most insurance coverage corporations have a most multiplier you may apply to your revenue for all times insurance coverage protection. For instance, it wouldn’t make a lot sense for a 22-year-old making $27,000 per 12 months to get a $2 million life insurance coverage. Or a 65-year-old that's retired to safe a $3 million greenback coverage.

The desk beneath is roughly how a lot you’re allowed to multiply your revenue based mostly in your age and revenue:

Applicant’s Age

Annual Earnings Multiplier

18-29

35x

30-39

30x

40-49

25x

50-59

20x

60-69

15x

70-79

10x

80+

5x

Utilizing the desk above as a information, a 35-year-old making $150,000 per 12 months could be capped at taking out a $4.5 million time period coverage ($150,000 x 30 = $4,500,000).

Your Ultimate Bills

Right here we begin with the fundamentals – wrapping up your last affairs.

Loopy, proper? You will get burial insurance coverage to cowl solely essentially the most fundamental of ultimate bills.

Excellent Debt

Debt burdens are excessive within the US, and debt might be particularly crushing on remaining relations. Many life insurance coverage prospects make certain they will repay most of their debt with the coverage.

Medical Debt

Medical prices are a severe variable. Even in case you have wonderful medical insurance, there are more likely to be unpaid medical payments lingering after your loss of life. This has to do with copayments, deductibles, and coinsurance provisions.

Collectively, they will add as much as many 1000's of {dollars}. However the place issues get actually sophisticated is should you die of a terminal sickness.

For instance, if you're affected by an sickness that lasts for a number of years, you possibly can incur quite a few bills that aren't lined by insurance coverage. This may occasionally embody the price of private care and even experimental remedies.

Mortgage

A house could also be a big asset, but it surely’s additionally usually a house owner’s largest debt. The typical mortgage stability within the US is roughly $236,443 in line with Experian information. So you possibly can simply use a life insurance coverage coverage to repay that debt and relieve your family members of a month-to-month mortgage fee.

Private Debt

Bank card debt and different private debt are a number of the costliest obligations carrying charges upward of 20% in some circumstances. Be sure to have sufficient to cowl this very costly debt.

Future Obligations For Your Household

Under is a sampling of main bills your loved ones is more likely to incur, both on an annual foundation or sooner or later after your loss of life.

School

Tuition prices proceed to skyrocket. The Division of Schooling means that four-year public faculty tuition has been rising a mean of 5% per 12 months, far exceeding the speed of inflation. When you've got one baby who attends an in-state public college, a second at an out-of-state public college, and a 3rd in a non-public college, the full expenditure will attain $416,560.

Annual value at in-state public faculty: $20,770 ($83,080 for 4 years)

Annual value at out-of-state public faculty: $36,420 ($145,680 for 4 years)

Annual value at a non-public faculty: $46,950 ($187,800 for 4 years)

Transportation

Autos and different types of transportation symbolize one other massive sum. Sadly, with rising electronics and security options, the typical value of a brand new automotive continues to develop.

Well being Insurance coverage

If your loved ones depends in your work for healthcare, take discover. In response to eHealth.com, the typical medical insurance premium for a household is $22,221. That’s a shade underneath $2,000 monthly in further value. This value will solely rise, and the necessity may final for years.

Different Obligations You Might Have to Cowl

Thus far, we’ve been describing the monetary obligations more likely to have an effect on a typical family. However there could also be sure conditions that may produce obligations which might be much less apparent.

Enterprise Homeowners

For instance, should you’re a enterprise proprietor, there could also be money owed or different monetary obligations that may must be paid upon your loss of life.

Although nobody in your loved ones could also be certified or curious about taking up your small business, the payoff of these obligations could also be utterly essential to allow the sale of the enterprise.

Actual Property Investor

One other chance is that you simply’re an actual property investor.

In case your properties are closely indebted, additional insurance coverage proceeds could also be vital both to hold the properties till they’re offered, and even to repay current indebtedness to liberate money movement for revenue.

It's possible you'll even want further funds if you're taking good care of an prolonged member of the family, like an ageing guardian.

These are simply a number of the many potentialities of bills that may must be lined by insurance coverage proceeds.

Elements Affecting Your Life Insurance coverage Premiums

Earlier than we transfer on to particular life insurance coverage quotes, let’s first think about the elements that have an effect on time period life insurance coverage premiums.

Age

That is usually the one most essential premium issue. The older you might be, the extra seemingly you might be to die throughout the time period of the coverage.

Well being

It is a shut second and why it’s so essential to use for a coverage as early in life as attainable. Premiums on life insurances charges actually improve by every year.

When you've got any well being circumstances which will have an effect on mortality, comparable to diabetes or hypertension, your premiums will probably be increased. That is one other compelling motive to use while you're younger and in good well being.

It’s not that insurance policies will not be out there to folks with well being circumstances, it’s simply that they’re cheaper should you don’t have any.

Coverage Time period

A ten-year time period coverage could have a decrease premium than a 20-year time period coverage, which will probably be decrease than a 30-year time period. The shorter the time period, the much less seemingly it's the insurance coverage firm must pay a declare earlier than it expires.

Coverage Dimension

Dimension of the coverage issues, however not the way in which you would possibly suppose. Sure, a $1 million coverage will value greater than a $500,000 coverage. But it surely received’t value twice as a lot.

The bigger the coverage, the decrease the per-thousand value will probably be.

When the dimensions of the loss of life profit is taken into account, the bigger coverage will all the time be cheaper.

Work, Hobbies, and Habits

For instance, sure occupations are extra hazardous than others (suppose policeman versus librarian). Deep-sea diving is increased danger than golf. And smoking is the one exercise assured to lift your premiums considerably.

With this data in thoughts, let’s check out whether or not it is best to think about a $1 million entire life coverage as an alternative.

$1 Million Time period Life Insurance coverage vs Complete Life?

Any dialogue on life insurance coverage ought to embody a comparability of entire life and time period life insurance coverage protection. In any case, each merchandise might be immensely helpful in the precise scenario, but one product (entire life) prices significantly greater than the opposite.

More often than not, the controversy is settled in favor of time period life insurance coverage based mostly on value alone.

An entire life insurance coverage coverage can simply value 10x the identical quantity of protection you will get with a time period coverage.

With that being mentioned, entire life insurance coverage and different investment-type life insurance coverage protection might be helpful when it comes to the money worth you may construct up over time. Complete life insurance coverage additionally affords a hard and fast profit quantity in your heirs that may final in your complete life, but the price of your premiums are assured to remain the identical.

The money worth of a complete life insurance coverage coverage additionally grows on a tax-deferred foundation, and you'll borrow in opposition to this quantity should you want a mortgage. Additional, many entire life insurance policies from respected suppliers additionally pay out dividends throughout good years, which might be substantial.

Why Younger Households Select Time period Protection

The issue with entire life and different related insurance policies like common life is the truth that premiums might be exorbitant for the quantity of protection you would possibly want.

A pair with younger youngsters supplies a great instance since they may want a $1 million greenback coverage or extra to offer revenue safety for his or her working years and have cash left for school tuition and different bills.

With younger households, bills are already excessive.

This consists of prices for meals for a household, childcare, heavy use of well being care, and the seemingly infinite demand for clothes, furnishings, and even leisure as the kids develop.

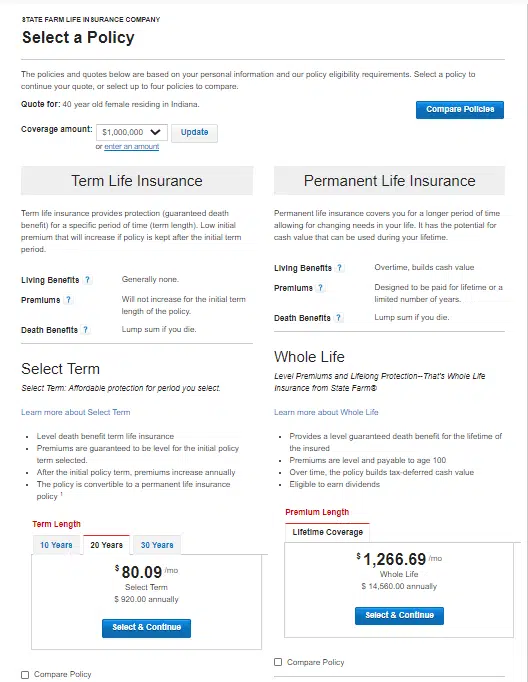

As you may see from the price comparability beneath from State Farm, there’s not sufficient room within the typical household funds to afford the sort of life insurance coverage that’s wanted.

A 40-year-old mom and breadwinner in wonderful well being would pay $80.09 monthly for a time period life coverage that lasts 20 years, whereas an entire life coverage in the identical quantity would value $1,266.69 monthly (or $14,560 yearly).

It is a basic scenario the place time period insurance coverage rides to the rescue. The household can afford to purchase the quantity of protection they want at an reasonably priced value, whereas paying for everlasting life insurance coverage protection in the identical quantity could be tough to justify.

And simply as essential for folks of any age and in any circumstance, the additional funds not being spent on insurance coverage premiums might be invested to step by step enhance your monetary scenario.

So completely, time period insurance coverage will work greatest for most individuals.

$1 Million Life Insurance coverage Fee Examples

As you’ll discover, every desk has a wide selection of data. Figuring out that everyone is in a unique scenario, I wished to guarantee that I provided time period life quotes for nearly each conceivable scenario.

For people who suppose {that a} million-dollar time period coverage is dear, you’ll shortly discover {that a} 25-year-old male in good well being solely prices $645 per 12 months whereas a 35-year-old prices $795.

On a month-to-month foundation that’s nearly subsequent to nothing!

AGE

SEX

COMPANY 1

COMPANY 2

COMPANY 3

25

MALE

BANNER LIFE $645

NORTH AMERICAN CO. $645

TRANSAMERICA $650

25

FEMALE

AMERICAN GENERAL $514

NORTH AMERICA CO. $515

SBLI $520

35

MALE

BANNER LIFE $795

GENWORTH FINANCIAL $804

ING $808

35

FEMALE

SBLI $640

AMERICAN GENERAL $694

GENWORTH FINANCIAL $695

45

MALE

BANNER LIFE $1,885

GENWORTH FINANCIAL $1891

AMERICAN GENERAL $1,894

45

FEMALE

SBLI $1,450

BANNER LIFE $1,455

AMERICAN GENERAL $1,456

20-Yr $1 Million Time period Life Coverage

There's a massive drop-off in life insurance coverage charges between a 20 12 months and a 30 12 months since underwriters should not have to fret as a lot about life expectancy.

For many individuals, a 20-year coverage will get them precisely the place they need to be in life when the coverage time period runs out.

AGE

SEX

COMPANY 1

COMPANY 2

COMPANY 3

25

MALE

AMERICAN GENERAL $414

BANNER LIFE $425

SBLI $440

25

FEMALE

AMERICAN GENERAL $354

SBLI $360

BANNER LIFE $365

35

MALE

SBLI $450

BANNER LIFE $455

NORTH AMERICA CO. $485

35

FEMALE

SBLI $390

AMERICAN GENERAL $404

BANNER LIFE $405

45

MALE

BANNER LIFE $1,155

SBLI $1,160

GENWORTH FINANCIAL $1,173

45

FEMALE

SBLI $880

BANNER LIFE $895

TRANSAMERICA $930

10-Yr $1 Million Time period Life Coverage

As soon as once more, you get a $200 drop within the annual premium by shedding one other 10 years on the time period.

In case your life insurance coverage agent isn’t providing you with all these time period choices and is barely targeted on the loss of life profit, then you definately want a unique agent.

AGE

SEX

COMPANY 1

COMPANY 2

COMPANY 3

25

MALE

SBLI $260

BANNER LIFE $285

MINNESOTA LIFE $290

25

FEMALE

SBLI $230

BANNER LIFE $245

ING $248

35

MALE

SBLI $270

BANNER LIFE $295

MINNESOTA LIFE $300

35

FEMALE

SBLI $240

BANNER LIFE $255

ING $258

45

MALE

BANNER LIFE $585

TRANSAMERICA $630

GENWORTH FINANCIAL $637

45

FEMALE

SBLI $520

BANNER LIFE $525

ING $528

$1 Million Coverage for People who smoke – Charges Improve

For all you people who smoke on the market – beware! The price of your life insurance coverage balloons as you’ll see right here. For those who’re contemplating kicking the behavior, now could be nearly as good time as any.

Some life insurance coverage corporations will provide you with a decrease fee should you full a acknowledged smoking cessation program, and go on with out smoking for not less than two years.

It received’t assist your fast scenario, however whenever you see the premium on smoker life insurance coverage charges beneath, you would possibly agree that it’s one thing to work towards!

AGE

SEX

COMPANY 1

COMPANY 2

COMPANY 3

35

MALE

North American Co. $3595

SBLI $3630

MetLife $3639

35

FEMALE

North American Co. $2555

Transamerica $2720

Prudential $2765

10 steps to securing one million life insurance coverage coverage:

For those who’ve made the choice that $1 million of life insurance coverage is the correct amount of protection you want and also you’re able to buy a coverage, listed below are the steps you’ll must comply with.

1. Decide How A lot Protection You Want: That is the primary and most essential step in securing one million life insurance coverage insurance policies. It's essential have a transparent understanding of how a lot protection you really need.

2. Select the Proper Kind of Coverage: There are entire life, time period life, and Common life insurance policies out there. Select the one which most accurately fits your wants.

3. Store Round: Don’t simply go together with the primary life insurance coverage firm you come throughout. It’s essential to check life insurance coverage charges and protection from a couple of totally different corporations earlier than making a choice.

4. Take into account Your Well being: For those who’re in good well being, you’ll seemingly qualify for decrease charges. Nonetheless, in case you have well being points, you should still be capable of get protection, however it is going to in all probability be dearer.

5. Take into account Your Way of life: When you've got a dangerous job or interest, that might have an effect on your charges.

6. Get Quotes From A number of Firms: That is one of the simplest ways to check charges and discover the most affordable coverage.

7. Learn the Fantastic Print: Be sure to perceive all of the phrases and circumstances of the coverage earlier than shopping for it.

8. Purchase On-line: You possibly can often get cheaper charges by shopping for life insurance coverage on-line.

9. Pay Consideration to Your Cost Schedule: Most life insurance coverage insurance policies require month-to-month or annual funds. Ensure you may afford the funds earlier than shopping for a coverage.

10. Overview Your Coverage Usually: Life modifications, and so do life insurance coverage wants. You'll want to assessment your coverage usually to ensure it nonetheless meets your wants.

Following these steps will assist you to get the very best fee on a million-dollar life insurance coverage coverage.

Be sure to perceive all of the phrases and circumstances earlier than signing on the dotted line. Additionally, make certain to buy round and evaluate charges from a number of corporations earlier than shopping for a coverage.

Sure, I do know I’ve mentioned that a couple of occasions on this article, but it surely’s price repeating. Many individuals go together with the primary life insurance coverage firm they name, and that isn’t form to their checkbook. It pays to buy round.

Right here’s what it is advisable to learn about selecting the most effective life insurance coverage firm in your $1 million coverage:

The Finest Firms to Buy $1 Million Life Insurance coverage

When selecting the most effective life insurance coverage firm, it’s essential to contemplate the general monetary well being of the insurance coverage firm. You need to make certain the corporate you select is steady and will probably be round for years to come back. You additionally need to think about issues like the corporate’s customer support score and claims-paying capacity.

There are plenty of totally different life insurance coverage corporations on the market, so it may be tough to know which one is the most effective. Every firm is rated by totally different organizations, so it’s essential to take a look at a number of rankings earlier than making a choice.

Score companies are the “Report Card” for all times insurance coverage corporations. Select an organization with straight A’s!

The businesses that fee insurance coverage corporations are A.M. Finest, Moody’s, and Normal & Poor’s.

A.M. Finest is a credit standing company that focuses on the insurance coverage business. They fee insurance coverage corporations on their monetary stability.

Moody’s is one other credit standing company. In addition they fee insurance coverage corporations on their monetary stability.

Normal & Poor’s is a credit standing company that charges corporations on their monetary stability.

The next life insurance coverage corporations are all rated A+ (Superior) by A.M. Finest and are thought of to be financially steady and have a great claim-paying capacity.

These are just some of the numerous life insurance coverage corporations on the market that might offer you a $1 million life insurance coverage coverage.

When selecting a life insurance coverage firm, it’s essential to contemplate their monetary stability, customer support score, and claims-paying capacity. The businesses listed above are all rated A+ (Superior) by A.M. Finest and are thought of to be financially steady with a great claims-paying capacity.

Northwestern Mutual, New York Life, MassMutual, Guardian Life, State Farm, Nationwide, USAA, MetLife, The Hartford, and Allstate are all good selections for all times insurance coverage corporations.

You possibly can’t put a value on peace of thoughts, and with a $1 million life insurance coverage coverage you may have the peace of thoughts realizing that your family members will probably be taken care of financially if one thing occurs to you.

Backside Line: How A lot Does A $1 Million Greenback Life Insurance coverage Coverage Value?

Getting a one-million-dollar time period life insurance coverage coverage is just not as costly as most individuals imagine. You can begin getting quotes at the moment from quite a lot of prime life insurers by deciding on your state from the map above.

Even those that go for the dearer everlasting life insurance coverage coverage will many occasions be stunned on the value.

Both approach, you will get these bigger quantities of protection and nonetheless not break the financial institution. However get your coverage now, whilst you’re nonetheless younger and in good well being.

FAQ’s on $1 Million Life Insurance coverage Coverage

How a lot does a $1,000,000 time period life insurance coverage coverage value?

The price of a $1,000,000 life insurance coverage coverage will differ based mostly on elements like your age, well being, and life-style. Nonetheless, you may count on to pay round $250 per 12 months for a wholesome 30-year-old. In response to Ladder Life, a $1 million time period life coverage for wholesome 30-year-old males prices round $2.08 per day.

How does a $1,000,000 time period life insurance coverage coverage work?

A $1 million time period life insurance coverage coverage is a sort of life insurance coverage that gives protection for a selected time period, often 10-20 years. For those who die in the course of the time period of the coverage, your beneficiaries will obtain a loss of life advantage of $1 million. For those who stay previous the time period of the coverage, the coverage will expire and you'll not obtain any loss of life profit.

A $1 million time period life insurance coverage coverage is an effective alternative for individuals who need to make certain their family members are taken care of financially if one thing occurs to them. It may also be a sensible choice for folks with plenty of debt, like a mortgage or pupil loans, that they need to make certain is paid off in the event that they die.

Can anybody purchase a million-dollar life insurance coverage coverage?

For essentially the most half, sure; however there are examples of people that can't purchase life insurance coverage. For example, folks with a terminal sickness or those that have been recognized with a life expectancy of fewer than two years will not be in a position to buy life insurance coverage insurance policies.

The opposite elements are your revenue, affordability, and suitability. For those who can't afford the premiums, then you definately will be unable to buy the coverage. And in case your revenue is say lower than $50,000 then the insurance coverage firm might not suppose it’s appropriate to buy a $1 million life insurance coverage coverage.

Is a million-dollar life insurance coverage price it?

One million-dollar life insurance coverage coverage might not be proper for everybody, however it may be a good suggestion in case you have plenty of debt or if you wish to make certain your loved ones is taken care of financially if one thing occurs to you.

Nobody likes to consider their loss of life, but it surely’s essential to have a life insurance coverage coverage in place in case one thing occurs to you. One million-dollar life insurance coverage coverage can provide you and the one you love’s peace of thoughts realizing that they are going to be taken care of financially if one thing occurs to you.

Who affords the most effective million-dollar life insurance coverage coverage?

There isn't any one-size-fits-all reply to this query, as the most effective coverage for you'll rely in your particular wants and preferences. Nonetheless, a number of the prime suppliers of million-dollar life insurance coverage insurance policies embody AIG, Banner Life, and Prudential. So be sure you discover your choices and evaluate quotes from totally different suppliers earlier than making a choice.

Do insurance coverage corporations supply million-dollar insurance coverage insurance policies with no medical examination?

Sure, insurance coverage corporations supply million-dollar insurance coverage insurance policies with no medical examination. Nonetheless, the premiums for these insurance policies are usually a lot increased than for insurance policies with a medical examination.

Most of us have a tendency to make use of single-use merchandise on a regular basis, however switching even a few of them out for sustainable merchandise meant to be reused time and again may help our planet. Plastic is piling up in landfills and oceans; it’s even floating round within the air. It is unhappy and irritating, and sadly, the issue cannot be solved by shoppers merely slicing down on single-use plastics—firms must do their half. However decreasing the quantity of rubbish we produce can provide us a way of company, to not point out you can save fairly a bit of cash by shopping for a product solely as soon as.

The most effective reusable merchandise are ones you are going to wish to use time and again. So in case you want the water bottles out of your favourite espresso chain or fancy handkerchiefs from an area boutique, that is what it’s best to get. And if in case you have a pile of disposable merchandise you wish to exchange, use them up first. That will help you get began, we have compiled a bunch of our favourite merchandise. Do not see something you want right here? Take a look at a few of our different roundups, just like the Greatest Eco-Pleasant Cleansing Merchandise, Greatest Recycled Luggage, Greatest Recycled Clothes, and for all the pieces else, Our Favourite Merchandise Manufactured from Recycled and Upcycled Supplies.

Up to date February 2024: We have added reusable baggies and lids from W&P, Friendsheep dryer balls, and Pacific eye masks.

Particular supply for Gear readers: Get a1-year subscription toWIREDfor $5 ($25 off). This consists of limitless entry to WIRED.com and our print journal (if you would like). Subscriptions assist fund the work we do on daily basis.

In mid-November 2021, an awesome storm begins brewing within the central Pacific Ocean north of Hawai‘i. Particularly heat water, heated by the solar, steams off the ocean floor and funnels into the sky.

This text is from Hakai Journal, a web based publication about science and society in coastal ecosystems.

A tendril of this floating moisture sweeps eastward throughout the ocean. It rides the winds for a day till it reaches the coasts of British Columbia and Washington State. There, the storm hits air turbulence, which pushes it into place—straight over British Columbia’s Fraser River valley.

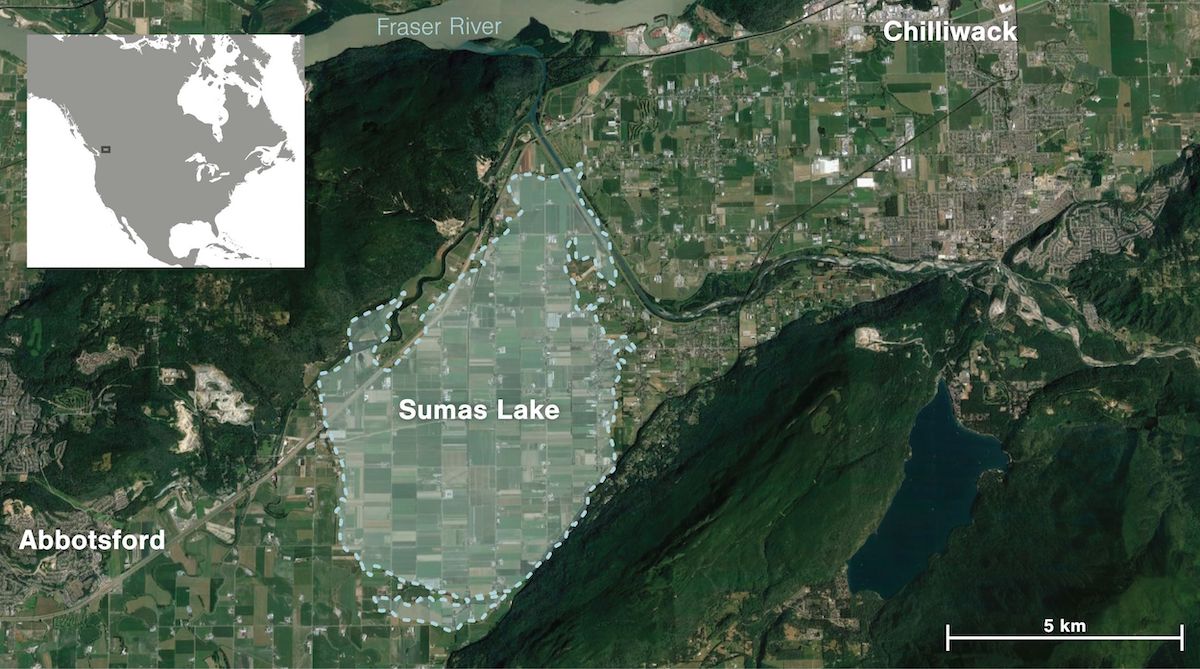

Clouds collect and darken. Beneath, a patchwork of farms and subdivisions sprawls alongside the Fraser River from its mouth, south of Vancouver, to the eastward mountain slopes, and southeast throughout the US border. On the middle of the valley lies Abbotsford, a metropolis of round 150,000 individuals nestled in a fingerprint-like melancholy between two mountains. Because the stream of humid air rises towards the peaks, it cools, condenses, and bursts.

To Murray Ned, it feels like a creek is overflowing outdoors his house in Kilgard, on a hillside inside Abbotsford that’s a part of the Semá:th (Sumas) First Nation reserve. Mendacity in mattress, Ned listens to water overflow his rain gutters and splash two tales to the bottom. Rain is frequent in Abbotsford in November, but it surely’s often quiet. And it often lets up.

Murray Ned stands on the fringe of his yard in Abbotsford, British Columbia, which was reworked into a ship launch following an unprecedented atmospheric river storm that dropped 172 millimeters of rain between November 13 and 15, 2021. (Jimmy Jeong)

Over the following two days, almost a month’s value of rain dumps right here and in different components of the province. The ensuing floods and landslides kill no less than six individuals, rip aside buildings, and buckle roads. In Abbotsford, greater than 1,000 houses are swamped and 640,000 cattle perish as rivers reclaim agricultural land within the floodplain.

However amid the losses, Ned sees one thing else. The Tuesday night of the flood—after he has vacuumed water from his mom’s basement and moved the household’s horses to excessive floor—the deluge stops. Ned settles right into a folding chair in his yard, pulls out a Kokanee lager, and takes within the view. The flood laps knee-high in opposition to his horse barn. Semá:th Xó:tsa, Sumas Lake, has returned to the territory.

As soon as a 6,475-hectare physique of water, Sumas Lake brimmed with sturgeon, trout, and 5 species of salmon—sustaining the Semá:th individuals and bigger Stó:lō Nation for millennia. The lake swelled with fall rains and spring snowmelt, and shrank throughout summer time, leaving fertile floor between the excessive and low water marks the place wild potatoes, berries, and blue camas flowers with edible bulbs thrived. By 1924, although, settlers had transformed the lakebed into everlasting farmland with a system of dikes, canals, and pumps. However after the 2021 storm, the whole lot within the lowlands is submerged once more, from cornfields to the Trans-Canada Freeway to a castle-themed enjoyable park.

Ned reveals how excessive the floodwaters rose round his horse barn after the mid-November 2021 atmospheric river rainstorm. (Jimmy Jeong)

Many of the floodwaters have come from the Nooksack River. Excessive runoff shifted the Nooksack’s course from its typical east–west movement in the US and despatched it speeding northward into Canada. Stó:lō elders know it might probably do that. For a lot of the postglacial interval, earlier than pure sedimentation deflected its course, the Nooksack fed the Sumas and Fraser Rivers in addition to Sumas Lake. Massive floods at the moment can nonetheless ship the river again north, borders be damned. Water was made to vary states. Not so way back, Sumas Lake had been there to catch it.

As Ned surveys the moonlit water, glistening round horse barns, poultry sheds, and energy strains, sturgeon and coho salmon swim outdated migration routes beneath the floor. “To see Mom Nature threaten [the region] but additionally see the lake in all its glory once more was fairly superb,” Ned tells me later. Alongside the lake, he sees the opportunity of a special future: one which restores area and adaptability for water and that retains communities safer from the extremes of local weather change.

The storm that hit Abbotsford is called an atmospheric river. These methods are frequent alongside the west coast of North America and midlatitudes world wide. They account for one-third to one-half of the annual precipitation in some areas and signify a serious supply of recent water for a lot of international locations. However research recommend that atmospheric rivers have gotten extra risky and are delivering water in greater bursts. Paradoxically, current storms, together with the one in British Columbia, have occurred between a few of the hottest and driest summers on report. After they ship wanted rain, it’s an excessive amount of for parched soils and concrete channels to include. This pendulum swing between deluge and drought—what meteorologists have began calling “climate whiplash”—will solely develop extra pronounced because the planet warms.

Ned and different members of Semá:th First Nation have begun advocating to revive no less than a part of Sumas Lake for the ecosystem and Stó:lō tradition, and likewise for flood management and pure water storage that can make the area extra resilient in opposition to future disasters. Up to now, they haven’t gained a lot traction in Abbotsford, however efforts elsewhere recommend they’re onto one thing. Maybe nowhere offers extra examples than California, which has lengthy ridden the seesaw between harmful downpour and punishing drought. Whether or not by foresight or give up, communities there are giving up new floor for water and restoring some pure methods, to work with rain when it comes.

Generally when heavy rain arrives in California, it originated close to Hawai‘i. Heat seawater evaporates and fills the air with water vapor, which will get blown throughout the Pacific till it collides with coastal mountains and falls as rain or snow. By the Nineteen Nineties, meteorologists believed {that a} windy layer within the decrease ambiance referred to as the low-level jet possible carried this tropical moisture. However simply how a lot moisture, how heat, how windy, and the place precisely it flowed remained mysterious.

In 1998, the Nationwide Oceanic and Atmospheric Administration got down to reply these questions with a program referred to as CALJET that deployed sensor-studded planes to fly into West Coast storms. By releasing devices referred to as dropsondes, which appear like mail tubes hooked up to small parachutes, the analysis group measured wind velocity, temperature, and moisture content material at completely different altitudes. A younger scientist named Marty Ralph directed the crew from the flight deck.

Ralph—who based and now directs the Heart for Western Climate and Water Extremes at Scripps Establishment of Oceanography on the College of California San Diego—first received curious about storms as a child dwelling in Arizona. He’d marvel from his bed room window on the monsoon rains that made the desert bloom. Later, as a graduate scholar on the College of California, Los Angeles, Ralph mounted a rain gauge outdoors his bungalow throughout one of many state’s worst droughts on report. He was shocked to seek out 100 millimeters of water within the gauge one winter night time; it ended up being half of the native rainfall for all the yr. “I received an early dose of how essential particular person storms may be in California,” Ralph says.

Marty Ralph, director of the Heart for Western Climate and Water Extremes at Scripps Establishment of Oceanography on the College of California San Diego, deplanes from a US Air Pressure C-130 “hurricane hunter.” This plane is utilized by the US authorities to forecast atmospheric rivers from the sky in actual time. (Erik Jepsen/UC San Diego)

On his CALJET flights, Ralph received to know these storms extra intimately, from their bumpy interiors and thick foggy cloaks to their distinct aroma that wafted by the aircraft’s air filters. “It smelled tropical,” Ralph recollects, “simply sticky and heat.” The scent was coming from distant. The truth is, satellite tv for pc pictures later revealed that the bands of water vapor stretched a few thousand kilometers from the tropics to the coast, and so they had been as large as the space between Vancouver, British Columbia, and Portland, Oregon. However essentially the most spectacular half was the moisture, or “juice,” that the dropsondes measured: “The equal of 25 Mississippi Rivers of water, however as vapor as a substitute of liquid,” Ralph says.

As soon as the group crunched the numbers, they discovered that their findings lined up with a couple of landmark research of the day. One, by researchers Yong Zhu and Reginald Newell, helped coin an evocative time period—atmospheric river. “That’s when the sunshine bulb went on,” Ralph says. “We had been finding out a river within the sky.”

Within the quarter-century for the reason that storms received their identify, researchers have discovered that on common a half-dozen of those methods are transferring moisture across the planet at any given time. Native monikers level to their origins: the Rum Runner sends juice from the Caribbean to western Europe; the Pineapple Categorical is the well-known rainmaker that whisks moist air from Hawai‘i to the West Coast. There, atmospheric rivers act like a touring sprinkler system, spraying up at Alaska in late summer time and swiveling right down to California by winter or spring.

These sprinklers are often useful, however as in British Columbia, they’ll grow to be hazardous cascades. Throughout California’s Nice Flood over the winter of 1861–1862, a collection of atmospheric rivers made it rain for 43 days. The floodwaters fashioned an inland sea that stretched from the under-construction capitol constructing in Sacramento to the underside of the traditional Tulare Lake basin within the Central Valley, and past. 1000’s of individuals and one-quarter of the state’s cattle died.

Paleo information from sediments present that atmospheric river–induced floods of no less than that magnitude have occurred in California roughly each 200 years over the previous two millennia. Right this moment, even storms lesser than these mega rains trigger 90 % of flood injury alongside components of the West Coast.

Residents of Sacramento, California, journey a predominant road by rowboat after a collection of atmospheric rivers beginning in December 1861 introduced 43 days of rain. (Courtesy of California State Library)

Atmospheric rivers additionally pummel the coasts of western Europe, Africa, South America, and New Zealand. They had been answerable for the horrific floods in Pakistan in August 2022 that killed almost 1,500 individuals and displaced 33 million extra. Their heat moisture is so good at liquefying snow and ice that they’re thawing components of Greenland and the Arctic. And since a hotter ambiance can maintain extra water vapor, local weather change is supercharging these storms. “You’ve got extra gas mainly,” Ralph says.

However on the identical time that rainfall is intensifying, the droughts that happen are deepening. California—which already faces essentially the most variable precipitation in the US—will possible see a future with fewer storms total and longer dry intervals between them. Mixed with the truth that the storms that do come are loaded with extra water, this implies the moist instances will get wetter and the dry instances will get drier. Extra of California’s water goes to pour down in floods.

“Flooding and drought actually are related,” says Michael Dettinger, a hydroclimatologist who’s been finding out atmospheric rivers alongside Ralph for the reason that mid-2000s. “One is simply the flip aspect of the opposite.”

California’s Lake Shasta, which feeds the Sacramento River, reveals naked banks in late October 2021. Amid the driest three-year interval since 1895, the reservoir dropped to lower than one-quarter of its water capability. (Andrew Innerarity/California Division of Water Sources)

Sacramento in mid-August 2022 is searing. It’s not simply the 40 °C temperature that’s setting information; California is about to shut out its driest three-year interval since 1895. In the summertime, the Sacramento Valley, a part of the bigger Central Valley that grows one-quarter of the US’ meals, is often a checkerboard of gold and inexperienced—the gold of spring wheat combined with glowing inexperienced stalks of sushi rice that sway within the heat breeze. However in 2022, Californian farmers planted lower than half the quantity of rice they projected. That’s as a result of there wasn’t sufficient water. Jacob Katz squints by his sun shades on the huge mud bowl that’s resulted. “Nobody has ever seen this earlier than,” he says, as we drive down a mud lane surveying the barren fields.

The senior scientist at California Trout, Katz has been working for greater than a decade to reconnect the Sacramento River—the state’s largest supply of recent water—to its adjoining floodplains. Just like the leaders of Semá:th First Nation to the north, Katz is aware of that making extra room for water may give the panorama and its inhabitants a buffer in opposition to climate whiplash.

Jacob Katz, the senior scientist at California Trout, factors to the place a passageway is being carved out of a levee on the Sacramento River to assist salmon and sturgeon attain the floodplain. (Joshua Asel)

On the finish of the street we’re touring is a working example: lifeless grass provides method to a watery oasis, glimmering like a mirage within the solar. Dozens of white-faced ibises dip and shimmy their wings whereas a sandpiper sips a cool drink. Inside minutes, an egret glides down from the hazy sky and sinks its black legs into the mud. All the life within the valley, it appears, is taking refuge on this shallow 55-hectare lake.

The “lake” is definitely a analysis plot at Davis Ranches, a heritage farm close to the Sacramento River that’s testing new approaches to water administration. One silver lining of the drought is that fallowed farmland can grow to be wildlife habitat, says the farm’s supervisor, John Brennan, who’s checking on the positioning with Sandi Matsumoto, water program director for the Nature Conservancy, a companion on this challenge. “We have to construct all of the habitat we will to prepare for the dry years,” Brennan says. That’s as a result of habitat can take in water when it’s accessible—ideally throughout floods—and retailer it within the soil and underground for people, crops, and animals to faucet into throughout dry spells.

White-faced ibises cool off in a flooded discipline at Davis Ranches, a heritage farm in California’s Sacramento Valley, in the summertime of 2022. Water from the Sacramento River is piped onto idle farmland right here to help threatened shorebirds and waders that migrate alongside the Pacific Flyway. (Joshua Asel)

This synthetic wetland was designed to help shorebirds that go to Sacramento throughout their annual migration from the Arctic to South America on a path often called the Pacific Flyway. Shorebirds have declined by about 40 % on the West Coast, and so they’re significantly susceptible to drought. However even seasonal habitat like this could make a giant distinction for birds, Matsumoto says. And it requires far much less water than rice farming.

The challenge is a summer time addition to what Davis Ranches and different farms already do for shorebirds and waterfowl in winter. After the rice harvest wraps within the fall, farmers deliberately flood their fields on the peak of the birds’ winter migration, when river water is extra considerable. If carried out at scale, this might cut back the flooding of some infrastructure and communities whereas permitting extra water to soak into the bottom, which in flip may also help help wildlife and people on the mercy of drought. “So we’ve these two issues: water insecurity and flood,” Katz says. “However they really have a standard resolution—puddles.”

Traditionally, when rain and snowmelt surged down from the Sierra Nevada—California’s craggy spine that, in moist years, is floor zero for atmospheric rivers—the Sacramento would generally swell to 70 instances its common movement and spill throughout a marshy mosaic that related to a wetland ecosystem bigger than the state of Connecticut. Tens of hundreds of thousands of birds and one of many world’s biggest chinook salmon runs relied upon these floodplains. However after the California gold rush, water engineers constricted the river between 1,600 kilometers of steep levees designed to blast floodwater straight to the ocean. Over the approaching many years, settlers changed the wetlands with farms and different developments.

Katz sums up that historical past in a single phrase: drainage. “We’re like anti-beavers,” he says. “In all places we go, we get water off the panorama as shortly as potential. It’s in our language: ‘drain the swamp.’ What does that imply? It means progress.”

In line with a rising physique of analysis, it additionally means extra intense flooding and drought. As a substitute of permitting water to unfold and seep into the earth, squeezing rivers between channels creates a superhighway for flood flows. And sending water away from the panorama means, for essentially the most half, the valley stays parched; below-ground aquifers wait desperately for drips. Add in the truth that agriculture pumps groundwater considerably sooner than these aquifers can recharge, and also you’ve received a really thirsty state. However mimicking the pure flows of water throughout the terrain may assist deal with each issues on the identical time.

Sandi Matsumoto, the water program director on the Nature Conservancy (pictured), and John Brennan, farm supervisor at Davis Ranches, are advocating for the way rice farming and wildlife habitat can coexist with added advantages for groundwater. (Joshua Asel)

“We have to return to the pure cycles of our system, which embrace atmospheric rivers, which embrace drought,” Matsumoto says. “We have to restore our pure methods which might be capable of take care of these extremes.”

She seems to be throughout the pop-up wetland the place dragonflies circle over neon-green algae. “Fish meals!” Katz declares. When daylight hits the shallow, nutrient-rich water, it blooms with phytoplankton and invertebrates, which then feed fish and birds. Efforts by teams just like the Nature Conservancy and California Trout to flood the valley in winter have been supporting dozens of species of birds, which, earlier than dropping off over the previous half-century, had been so quite a few they’d black out the solar.

Native fish, like endangered winter-run chinook salmon, additionally profit after they have entry to meals and shelter on the floodplain. Analysis reveals that juvenile chinook launched into wetlands can develop 5 instances sooner than these confined to a channel between levees. They’re extra more likely to survive their odyssey to the ocean and again as properly. “It’s night time and day,” Katz says. Straitjacketed rivers with managed flows favor fish like bass which might be invasive in California. However pure swings and flood occasions help the native salmon they’ve formed, similar to they’ve formed this fertile valley. “Flood doesn’t must be catastrophic,” Katz says. “It may also be a driver of the productiveness and abundance we so worth.”

Releasing rivers has been catching on as a flood mitigation technique round North America and the world. And the locations welcoming water are seeing added advantages.

Within the Netherlands, a program referred to as Room for the River has eliminated dikes and created aspect channels for water and fish to meander by 34 riverside communities. Many of those locations now provide higher biodiversity and recreation along with enhanced flood security. The brand new shops for water act like pressure-release valves when flows are excessive. Throughout a freak summer time flood on the Meuse river in 2021, water ranges had been the best ever recorded in some locations. However downstream, thanks partly to those Room for the River tasks, there was a lot much less flood injury than in earlier years, even with greater flows.

An identical program in Washington State has restored 114 kilometers of fish habitat and created greater than 3,700 jobs, starting from outreach employees to engineers. Within the state’s southwest nook, alongside the Columbia River, locals are additionally flattening levees to present lamprey and salmon year-round entry to 370 riparian hectares whereas additionally defending infrastructure from flooding.

Whereas California’s plumbing is extra advanced—it’s probably the most engineered water methods on the planet—the state can also be restoring some riverways. On the Sacramento, for instance, employees are digging 15,000 dump vans’ value of earth from a levee in order that salmon and sturgeon have a greater likelihood of reaching the floodplain. And now, due to rising consciousness of atmospheric rivers and precipitation swings, water managers are beginning to perform floodplain tasks particularly to spice up groundwater: a near-miraculous co-benefit.

The California Aqueduct carries water from wetter Northern California to the arid reaches of the San Joaquin Valley and Los Angeles. It’s the snaking central artery of the 1,135-kilometer State Water Undertaking—one of many largest water conveyance methods on the planet. (iofoto/Shutterstock)

The final discipline we go to at Davis Ranches crunches with dry grass and weeds, one other casualty of the drought. However the earlier December, an atmospheric river unloaded a great quantity of rain. This 24-hectare tract was ready for the deluge. The ranch piped floodwater from the river into this plot, and its porous soils sucked it up like a sponge. Over a couple of weeks, the sponge trickled its contents by sand, silt, and gravel into layered swimming pools within the earth: groundwater aquifers. On the identical time that puddles had been feeding stilts and sandpipers above floor, the water desk beneath was rising.

This means of sending floor water underground just isn’t a brand new concept, however the drought has given it new urgency together with a brand new identify: managed aquifer recharge, often known as MAR, Ag-MAR, or Flood-MAR. With most river water already rationed amongst human makes use of, in addition to minimal flows for fish, extra water from atmospheric rivers may be the shock absorber between flooding and drought if allowed to pool on the land as a substitute of charging out to sea. “The one water not spoken for is these flood flows,” Brennan says. “Even within the driest years, we’ve additional water.”

Since beginning the recharge challenge in 2019, Davis Ranches has captured about 370,000 cubic meters of water every winter. That’s round what 150 US households use in a yr, and it’s simply from one discipline, overlaying just one % of this property. The farm is saving up that groundwater to share with neighbors at a later date, with the aim of leaving extra water on the floor for wildlife.

In essentially the most drought-prone reaches of the state, communities are equally turning to groundwater recharge, usually placing pipes and canals arrange for summer time irrigation to new use throughout winter to divert flood flows into aquifers. By 2022, native governments in areas the place human use has depleted aquifers had been required to submit sustainability plans in accordance with a 2014 state legislation geared toward restoring groundwater. Many of those plans embrace recharge tasks just like the one at Davis Ranches however bigger.

The California Aqueduct carries water from wetter Northern California to the arid reaches of the San Joaquin Valley and Los Angeles. It’s the snaking central artery of the 1,135-kilometer State Water Undertaking—one of many largest water conveyance methods on the planet. (iofoto/Shutterstock)

The California Division of Water Sources (DWR) has already invested US $68 million into 42 of those tasks, transferring one-quarter of the way in which towards governor Gavin Newsom’s aim of increasing recharge capability within the state by greater than 616 million cubic meters. That’s the equal of including one other massive reservoir however underground, protected from warmth and evaporation. By some estimates, the sapped aquifers beneath the Central Valley have area for 3 times extra water than all of California’s reservoirs mixed. DWR is now vetting dozens of further tasks geared toward banking water beneath floor.

The summer time I go to the Sacramento Valley is the primary summer time after the devastating storm in Abbotsford. Regardless of the town rebuilding a destroyed part of dike, water from the Sumas River nonetheless seeps by the reinforcements right into a cattle farm. The flooded space has shrunk to the dimensions of some soccer fields, however its water nonetheless teems with geese and geese. To the Semá:th individuals, it nonetheless carries the spirit of Sumas Lake.

Traditionally, Sumas Lake would have been this small solely throughout a serious drought. However even with out the pure lake as an indicator, indicators of dry instances are cracking by the panorama. In 2022, the city of Chilliwack, simply up the Fraser River from Abbotsford, has recorded the most popular August and September in additional than 140 years. And whereas Abbotsford—which depends on some groundwater for consuming—has a number of steady aquifers, the area can also be house to the one two aquifers identified to be declining close to the southern coast of British Columbia. (Aquifers are additionally essential for replenishing native streams and rivers from beneath floor throughout summer time.) And whereas drought could also be extra refined right here than it’s in California, scientists challenge that components of the province are due for warmer and longer dry spells between downpours, too.

In September 2022—10 months after the most expensive flood in BC historical past—a small remnant lake nonetheless covers farmland in Abbotsford. It attracts geese and geese to forage alongside its edges. (Serena Renner)

The truth that his house feels distinctly “droughty” so quickly after the most expensive flood in BC historical past issues Murray Ned. “For me and my technology, we might not must endure it an excessive amount of,” he says. “However for my grandchildren, my children … Yeah, it’s very alarming.”

As govt director of the Decrease Fraser Fisheries Alliance and an adviser to Semá:th First Nation, the place he served as a councilor for 25 years, Ned is very involved about culturally essential sturgeon and salmon. They’ve been lower off from round 85 % of their floodplain habitat, which traditionally included Sumas Lake. Coho, chum, and chinook salmon nonetheless migrate to the world to spawn, together with sturgeon, however all these species are in decline. Warming water and drought are including new pressures. In line with scientists and Semá:th leaders, reviving Sumas Lake may assist.

Earlier than it was absolutely drained in 1924 for farmland by new settlers to British Columbia, Sumas Lake unfold between Sumas and Vedder Mountains to the north and south, respectively. It served because the cultural and financial lifeblood of the Semá:th individuals and bigger Stó꞉lō Nation. (Graphic by Mark Garrison, based mostly on picture from Google Earth)