[ad_1]

LIC is launching its new pension plan Jeevan Dhara 2 (No.872) on twenty second January 2024. Do you have to make investments on this GUARANTEED new pension plan of LIC?

LIC Jeevan Dhara 2 is a pension plan that GUARANTEES a hard and fast earnings to your retirement. It gives life cowl solely in the course of the deferment interval and provides each single and common premium choices. Moreover, present LIC policyholders, nominees, or beneficiaries can take pleasure in enhanced advantages of this plan.

Do do not forget that it is a deferred annuity plan however not an instantaneous annuity plan. Earlier than continuing additional, first, allow us to perceive few terminologies utilized in retirement plans.

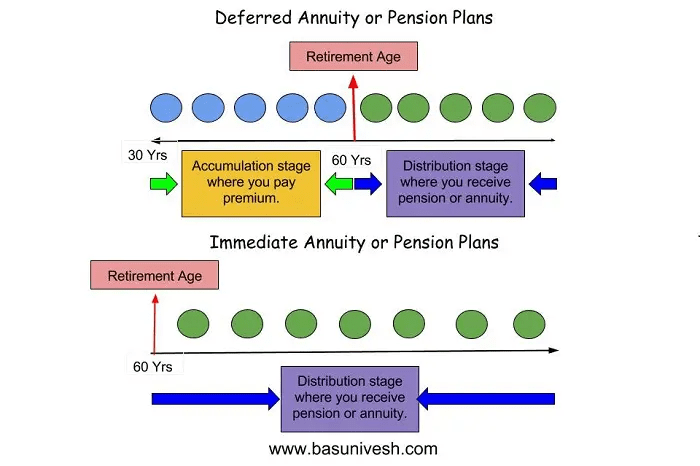

In easy phrases, you’ll be able to say it’s a Pension, the place you’ll get common earnings as much as the desired interval or circumstances. There are two sorts of annuity.

1) Rapid Annuity-On this case, you make investments a lump sum in a product and your pension or annuity begins instantly. Allow us to say you could have round Rs.1 Cr and if you happen to purchase fast annuity plans, then the pension will begin instantly from subsequent month.

2) Deferred Annuity-On this case your annuity begins after a sure interval. Allow us to say your present age is 30 years and you’re planning to retire on the age of 60 years. When you purchase a deferred annuity plan, then you’ll make investments as much as your retirement age i.e. as much as 60 years of age. After 60 years of retirement, your pension will begin.

I attempted to elucidate the identical with under illustration under.

As I discussed above, LIC New Pension Plan Jeevan Dhara 2 is a deferred annuity plan however not an instantaneous annuity plan.

LIC New Pension Plan Jeevan Dhara 2 – Options and Eligibility

Allow us to see the options of LIC New Pension Plan Jeevan Dhara 2 options and eligibility.

| LIC New Pension Plan Jeevan Dhara 2 Options (www.basunivesh.com) |

|

| Minimal Age At Entry | 20 Yrs |

| Most Age At Entry | Choice – 1,2,8,9 (10 & 11- Single Premium) – 80 Yrs minus Deferrment Interval. Choice – 5,6 & 7 – 70 Yrs minus Defferment Interval Choice – 3 & 4 – 65 Yrs minus Defferment Interval Choice – 8 & 9 (Secondary Annuitant) – 75 Yrs Choice – 11 (Single Premium Secondary Annuitant) – 79 Yrs |

| Minimal Vesting Age | Choice – 1 to 9 – 35 Yrs Choice – 10 and 11 – 31 Yrs |

| Most Vesting Age | Choice – 1,2,8,9 (10 & 11- Single Premium) – 80 Yrs Choice – 5,6 & 7 – 70 Yrs Choice – 3 & 4 – 65 Yrs |

| Defferment Interval | Choice – 1 to 9 – 5 to fifteen Yrs Choice – 10 and 11 – 1 to fifteen Yrs |

| Premium Cost Time period and Mode | Common (Yrly, Hly, Qtly and Mnthly (Equal to defferment Interval) and Single |

| Pension Cost Mode | You may pay a further premium to high up your advantages. The charges will likely be based mostly on the prevailing annuity charges. Every such top-up is handled as a single coverage for advantages. |

| Minimal Pension | Yrly – Rs.12,000, Hly – Rs.6,000, Qtly – Rs.3,000 and Month-to-month – Rs.1,000 |

| Prime Up Facility | Obtainable just for RETURN OF PREMIUM choices (Choices 2,9,10 and 11) You may avail of it after the 5 years of graduation of pension. Max 3 instances you’ll be able to withdraw. Withdrawal should not exceed 60% of the full premiums paid. |

| Liquidity | Obtainable just for Return of Premium Choice or Buy Value. |

| Incentive for Policyholders/Nominees/Beneficiary | Obtainable just for OFFLINE buy coverage. 0.5% enhance in pension – For normal premium 0.25% enhance in pension – For single premium |

| Mortgage | Obtainable just for Return of Premium Choice or Buy Value. Mortgage could be availed throughout or after the deferment interval. |

Be aware – You may give up at any cut-off date for the insurance policies of a single premium. Nevertheless, for normal premiums, give up is out there throughout or after the deferment interval if you happen to paid not less than 2 years of premium.

Under are the pension or annuity choices one can select from LIC New Pension Plan Jeevan Dhara 2.

| LIC New Pension Plan Jeevan Dhara 2 Annuity Choices (www.basunivesh.com) |

|

| Common Premium Single Life | Choice 1 – Life annuity for single Choice 2 – Life annuity with return of premium Choice 3 – Life annuity with 50% of the return of premium after 75 Yrs Choice 4 – Life annuity with 100% return of premium after 75 Yrs Choice 5 – Life annuity with 50% of the return of premium after 80 Yrs Choice 6 – Life annuity with 100% return of premium after 80 Yrs Choice 7 – Life annuity with 5% return of premium after 76 Yrs to 95 Yrs |

| Common Premium Joint Life | Choice 8 – Life annuity for joint life Choice 9 – Life annuity with return of premium for joint life |

| Single Premium Single Life | Choice 10 – Life annuity with return of ourchase value |

| Single Premium Joint Life | Choice 11 – Life annuity with return of buy value |

LIC New Pension Plan Jeevan Dhara 2 Loss of life Advantages

# Single Life (Choices 1 to 7 and 10)

Loss of life in the course of the deferment interval -105% of the full premiums paid as much as the date of the demise will likely be payable to the nominee.

Loss of life throughout pension fee interval – Pension will cease instantly. No demise advantages if you happen to opted for the choice of an annuity with out the return of a premium. When you go for the return of buy value, 100% of the full premium paid will likely be payable to the nominee. Nevertheless, if you happen to opted for the return of premium beneath choices 3 and seven and demise occurs at 75,80, or between 76 to 95 years of age, then the nominee will obtain 100% of the full premium paid minus the sum of early return of premium already paid until the date of demise.

# Single Life (Choices 8,9 and 11)

Loss of life in the course of the deferment interval – On the primary demise of both of the policyholders, there is not going to be any demise profit and the coverage will proceed as ordinary. Nevertheless, on the demise of the final survivor, demise advantages equal to 105% of the full premiums paid as much as the date will likely be payable to the nominee.

Loss of life throughout pension fee interval – On the primary demise of both of the policyholders, there is not going to be any demise profit and coverage profit will likely be payable to the survivor. Nevertheless, on the demise of the final survivor, beneath possibility 8, no demise profit will likely be payable. However beneath the 9 and 11 annuity choices, 100% of the full premium paid is payable to the nominee.

LIC New Pension Plan Jeevan Dhara 2 – Ought to You Make investments?

- As it’s a deferred non-linked annuity plan, you’ll be able to name it a typical TRADITIONAL PLAN of LIC.

- Then what’s GUARANTEED right here? The pension you’ll get a post-deferment interval is assured. It means you’re certain of how a lot pension you’ll get.

- Look at the out there pension choices extra intently and you’ll discover that all of them provide a hard and fast pension quantity, though with slight variations. Nevertheless, this strategy fails to think about the potential results of inflation in your retirement funds. To handle this, you haven’t any possibility however to speculate extra to maintain your retirement with rising inflation.

- The second greatest drawback is as that is an annuity plan, the pension you obtain throughout your retirement is taxable earnings and taxed as per your tax slab.

- LIC has launched extra pension choices that weren’t out there in its earlier plans, such because the return of premium in the course of the pension interval at a selected age. This gives some reduction for pensioners by way of bills like healthcare. Nevertheless, as talked about earlier, it doesn’t deal with the problem of inflation. Although Choice 7 permits for a 5% premium payout from 76 to 95 years (along with common premiums), the annuity charge is probably going decrease than the straightforward annuity for all times possibility.

- In an try to draw present policyholders and their beneficiaries, LIC has launched one other tactic by offering incentives within the type of pension advantages. Nevertheless, these advantages look like insignificant. Moreover, these advantages are completely out there for offline purchases, indicating a technique to spice up gross sales by means of brokers.

- In case you are keen to miss the affect of inflation in your retirement funds, have a robust religion in LIC, anticipate decrease inflation throughout your retirement, and rely partially on this product to your retirement, then this coverage is an possibility for you.

- Do do not forget that the above submit is written based mostly on the options however doesn’t take into account the annuity charge. Nevertheless, even when the annuity charges are good (in comparison with different insurers), I strongly counsel you to keep away from such GUARANTEED merchandise.

[ad_2]