[ad_1]

{kind=link}

By Sean Kevelighan, Triple-I CEO

Laws proposed by U.S. Rep. Adam Schiff (D-Calif.) to create a federal “disaster reinsurance program” raises a number of considerations that warrant scrutiny and dialogue – beginning with the query: Does what’s being proposed even qualify as insurance coverage?

If enacted into legislation, the invoice would set up a “catastrophic property loss reinsurance program…to supply reinsurance for qualifying major insurance coverage firms.” To qualify, insurers must provide:

- An all-perils property insurance coverage coverage for residential and business property, and

- A loss-prevention partnership with the policyholder to encourage investments and actions that scale back insured and financial losses from a disaster peril.

The proposed program would section in protection necessities peril by peril over a number of years and discontinue FEMA’s Nationwide Flood Insurance coverage Program (NFIP). It might set protection thresholds and dictate ranking elements primarily based on enter from a board wherein the insurance coverage business is just nominally represented.

And nowhere within the 22-page proposal do any of the next phrases or phrases seem:

- “Actuarial soundness”;

- “Danger-based pricing”;

- “Reserves”; or

- “Policyholder surplus”.

Actuarially sound risk-based pricing and the necessity to keep ample reserves and policyholder surplus to make sure monetary power and claims-paying means are the bedrock of any insurance coverage program worthy of the identify – not technical superb print to be labored out down the street whereas present mechanisms are being dismantled and market forces distorted by way of authorities involvement.

Insurance coverage is a sophisticated self-discipline, and prior federal makes an attempt at offering protection have struggled to steadiness their purpose of accelerating availability and lowering premiums in opposition to the necessity to base underwriting and pricing on actuarially sound rules to make sure enough reserves for paying claims.

Actuarially sound risk-based pricing and the necessity to keep ample reserves and policyholder surplus…are the bedrock of any insurance coverage program worthy of the identify – not technical superb print to be labored out down the street…

Sean Kevelighan, CEO, Triple-I

Be taught from historical past

NFIP is a robust working example. Created in 1968 to guard property homeowners for a peril that almost all non-public insurers had been reluctant to cowl, NFIP’s “one-size-fits-all” strategy to underwriting and pricing has led to this system now owing greater than $20 billion to the U.S. Treasury as a result of it lacked the reserves to totally pay claims after main occasions like Hurricane Katrina and Superstorm Sandy. It additionally typically led to lower-risk property homeowners unfairly subsidizing protection for higher-risk properties.

Having thus realized the significance of risk-based pricing, NFIP has modified its underwriting and pricing methodology. The brand new strategy – Danger Ranking 2.0, introduced in 2019 and totally carried out as of April 1, 2023 – extra equitably distributes premiums primarily based on house worth and particular person properties’ flood danger. Because of this, premiums of beforehand sponsored policyholders – significantly in coastal areas with increased values – have risen, resulting in outcries from many higher-risk homeowners who’ve seen their subsidies diminished.

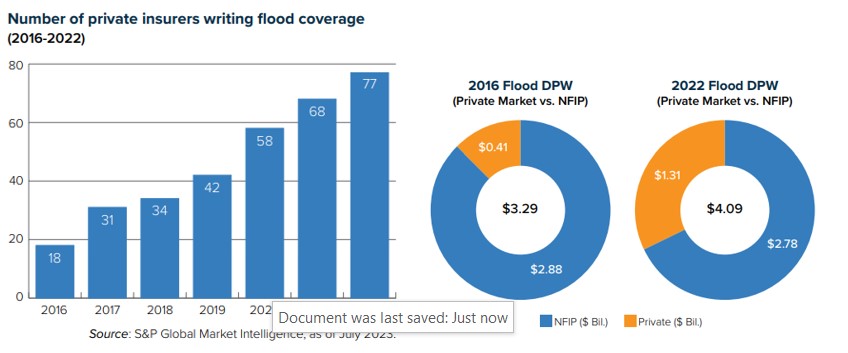

Along with resulting in fairer pricing, Danger Ranking 2.0 – by lowering market distortions – will increase incentives for personal insurers to get entangled. For a very long time, non-public insurers thought-about flood an untouchable peril, however improved knowledge modeling and analytical instruments have elevated their consolation penning this enterprise. Because the charts under present, non-public insurers have been enjoying a steadily rising position lately, masking a bigger proportion of a rising danger pool.

Over time, this development ought to result in higher availability and affordability of flood insurance coverage protection.

Somewhat than incorporating the teachings generated by NFIP’s expertise with a single peril, Rep. Schiff’s proposal would discontinue the reformed flood insurance coverage program whereas including a brand new layer of complexity to protection throughout all perils and casting into query the way forward for numerous state insurance coverage applications and residual market mechanisms at present in place.

Time-tested rules

Any try by the federal authorities to deal with insurance coverage availability and affordability considerations have to be made with an understanding of how insurance coverage works – from pricing and underwriting to reserving and declare settlement. For instance, the Schiff invoice proposes piloting an all-perils coverage with a time period of 5 years. There are good causes for property/casualty insurance policies to be written with a one-year time period. Particularly, the circumstances that have an effect on claims prices can change rapidly, and insurers – as referenced above – should put aside enough reserves to have the ability to pay all professional claims. If they can’t revisit pricing yearly, the monetary outcomes could possibly be disastrous.

“Who would have thought in 2019 that substitute prices would improve 55 p.c inside three years?” requested Dale Porfilio, Triple-I’s chief insurance coverage officer. Provide-chain disruptions associated to the COVID-19 pandemic and Russia’s invasion of Ukraine contributed to only such a replacement-cost spike. “Requiring five-year phrases for insurance policies would have led to an enormous drain on policyholder surplus.”

Policyholder surplus is the monetary cushion representing the distinction between an insurer’s belongings and its liabilities.

In saying his proposed laws, Rep. Schiff stated it’s meant to “insulate customers from unrestrained price will increase by providing insurers a clear, pretty priced public reinsurance various for the worst climate-driven catastrophes.”

This language ignores the truth that, below state-by-state regulation, premium fee will increase are something however “unrestrained” and ratemaking relies on actuarially sound rules which can be clear and honest. Property/casualty insurance coverage already is among the most closely regulated industries in america.

Customers deserve actual options

Policyholders have professional considerations about affordability and, in some instances, availability of insurance coverage. These considerations can create stress for political leaders at each the state and federal ranges to advance measures which can be perceived as promising to assist. Sadly, many latest proposals start by mischaracterizing present tendencies as an “insurance coverage disaster,” versus what they actually characterize: A danger disaster.

Insurance coverage premium charges have a tendency to maneuver in keeping with the frequency and severity of the perils they cowl. In addition they are affected by elements like fraud and litigation abuse; local weather, inhabitants, and growth tendencies; and world economics and geopolitics. That’s the reason insurers rent actuaries and knowledge scientists and make use of cutting-edge modeling expertise to make sure that insurance coverage pricing is actuarially sound, honest, and compliant with regulatory necessities in all states wherein they do enterprise.

That’s how insurers maintain lower-risk policyholders from unfairly subsidizing higher-risk ones.

To its credit score, the federal authorities is working to cut back climate-related dangers and investing in resilience by way of applications like Neighborhood Catastrophe Resilience Zones (CDRZ) and FEMA’s Constructing Resilient Infrastructure and Communities (BRIC) program. The Bipartisan Infrastructure Legislation comprises substantial funding to advertise local weather resilience. These are worthy endeavors geared toward addressing dangers that drive up insurance coverage prices.

However historical past has proven that direct authorities involvement within the underwriting and pricing of insurance coverage merchandise tends to not finish nicely. Any plan that might try and micromanage insurers’ protection of all perils by way of a lens that ignores time-tested, actuarially sound risk-based pricing rules raises a number of purple flags that have to be mentioned and addressed earlier than such a plan is allowed to change into legislation.

Be taught Extra:

It’s Not an “Insurance coverage Disaster” — It’s a Danger Disaster

Miami-Dade, Fla., Sees Flood Insurance coverage Price Cuts, Due to Resilience Funding

Matching Worth to Peril Helps Hold Insurance coverage Out there and Reasonably priced

Policyholder Surplus Issues: Right here’s Why

Triple-I Points Transient: Flood

Triple-I Points Transient: Proposition 103 and California’s Danger Disaster

Triple-I Points Transient: Danger-based Pricing of Insurance coverage

Triple-I Points Transient: How Inflation Impacts P/C Insurance coverage Pricing – and How It Doesn’t

Triple-I Points Transient: Race and Insurance coverage Pricing

[ad_2]